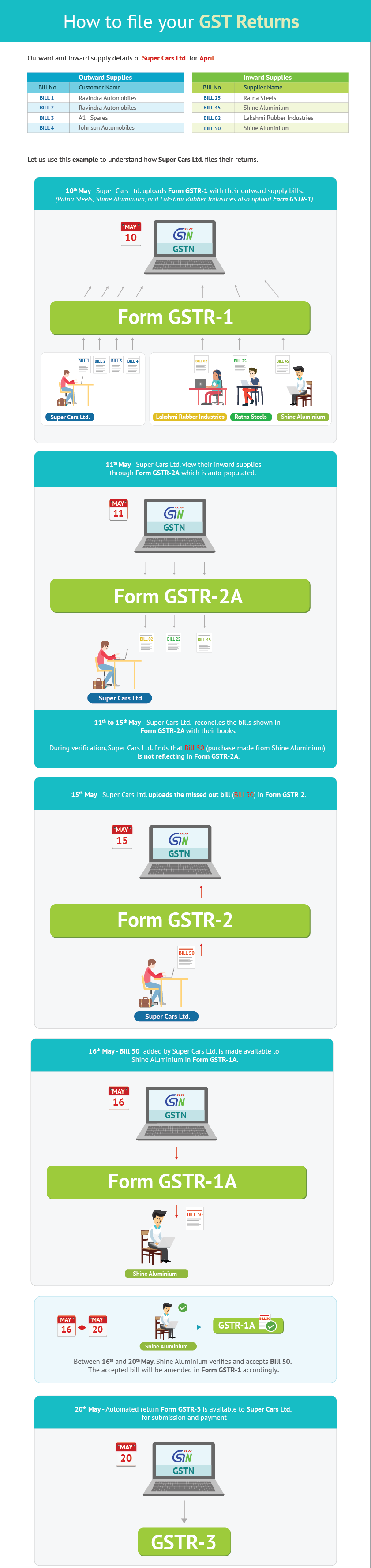

Invoicing is a crucial aspect of tax compliance for every business. It is essential to be aware of the rules of invoicing under GST. Let us understand these in detail.

Invoicing in the current tax regimes

In the current tax regimes, tw

o types of invoices are issued:

- Tax invoice – This is issued to registered dealers, and can be used to claim tax credit. Sample formats of the two main types of tax invoice in the current tax regime, the Rule 11 Excise invoice and tax invoice are shown below.

- Retail or commercial invoice – This is issued to an unregistered dealer or retail customer, and no tax credit can be claimed on this invoice. Sample format of a retail invoice in the current tax regime is shown below.

Invoicing in the GST regime

In the GST regime, two types of invoices will be issued:

- Tax invoice

- Bill of supply

Tax invoice

When a registered taxable person supplies taxable goods or services, a tax invoice is issued. Based on the rules regarding details required in a tax invoice, a sample tax invoice has been shown below.

What is the time limit for issue of tax invoice?

| Supply of goods | The tax invoice must be issued before or at the time ofRemoval of goods, where supply involves movement of goods

E.g. – When Super Cars Ltd, a car manufacturer, supplies cars to its dealer Ravindra Automobiles, the invoice must be issued at the time of removal of the cars from Super Cars Ltd’s premises. This is because the supply involves movement of the cars to Ravindra Automobiles’ premises. OR Delivery of goods to the recipient, where supply does not require movement of goods E.g. – Super Cars Ltd purchases a generator set, which will be assembled and installed at the factory premises by the supplier. Here, since the supply does not require movement of the generator set, the invoice must be issued at the time when the generator set is made available to Super Cars Ltd. |

| Supply of services | The tax invoice must be issued within 30 days from the date of supply of the service. Where the supplier is a bank or any financial institution, the invoice must be issued within 45 days of the supply of service. |

Note: In case a person paying tax on reverse charge receives goods or services from an unregistered supplier, the receiver must issue an invoice on the date of receipt of goods or services.

How many copies of the tax invoice are required?

For supply of goods, three copies of the invoice are required – Original, Duplicate, and Triplicate.

Original invoice: The original invoice is issued to the receiver, and is marked as ‘Original for recipient’.

Duplicate copy: The duplicate copy is issued to the transporter, and is marked as ‘Duplicate for transporter’. This is not required if the supplier has obtained an invoice reference number. The Invoice reference number is given to a supplier when he uploads a tax invoice issued by him in the GST portal. It is valid for 30 days from the date of upload of invoice.

Triplicate copy: This copy is retained by the supplier, and is marked as ‘Triplicate for supplier’.

For supply of services, two copies of the invoice are required:

- Original Invoice: The original copy of the invoice is to be given to receiver, and is marked as ‘Original for recipient’.

- Duplicate Copy: The duplicate copy is for the supplier, and is marked as ‘Duplicate for supplier’.

What details must a tax invoice for export contain?

An export invoice must, in addition to the details required in a tax invoice, contain the following details:

| Export invoice |

|---|

| Must have the words ‘“Supply meant for export on payment of IGST†or “Supply meant for export under bond without payment of IGST†|

| Name and address of the recipient |

| Delivery address |

| Number and date of ARE-1 (application for removal of goods for export) |

Bill of Supply

Bill of Supply is to be issued by a registered supplier in the following cases:

- Supply of exempted goods or services

- Supplier is paying tax under composition scheme

Based on the rules regarding details required in a Bill of supply, a sample Bill of Supply has been shown below.

The bill of supply need not be issued when the value of goods or services supplied is less than Rs 100, unless the receiver insists for the bill. However, a consolidated bill of supply should be prepared at the end of the business day for all such supplies for which the bill of supply is not issued.

How to revise the values of an invoice already issued?

To revise the taxable value or GST charged in an invoice, a debit note or supplementary invoice or credit note must be issued by the supplier.

Debit note/supplementary invoice- These are to be issued by a supplier to record increase in taxable value &/or GST charged in the original invoice.

Credit note- These are to be issued by a supplier to record decrease in taxable value &/or GST charged in the original invoice. Credit note must be issued on or before 30th September following the end of the financial year in which the supply was made OR the date of filing of the relevant annual return, whichever is earlier.

Let us understand the time limit for issue of credit note with an example.

Example

Super Cars Ltd sells spare parts worth Rs. 6,00,000 to its dealer Ravindra Automobiles on 1st November ‘17.  On 2nd November ’17, Ravindra Automobiles returned spare parts worth Rs 1,00,000, being damaged goods. Super Cars Ltd wants to raise a credit note for the goods returned.

Let us ascertain the last date by when Super Cars Ltd must issue the credit note using 2 scenarios-

Scenario 1- They file annual return of the Financial Year 17-18 on 1st December ‘18

Scenario 2- They file annual return of the Financial Year 17-18 on 31st May ‘18.

| Scenario | Date of original supply | Annual return filing date | Condition for determining last date to issue credit note | Last date for issuing credit note |

|---|---|---|---|---|

| Scenario 1 | 1st November 2017 | 1st December ‘18 | 30th September following the end of the financial year in which the supply was made or the date of filing annual return, whichever is earlier | 30th September ‘18 |

| Scenario 2 | 31st May ‘18 | 31st May ‘18 |

What details should debit notes, supplementary invoices and credit notes include?

Debit notes, supplementary invoices and credit notes must include the following details:

| Debit note/Supplementary Invoice/Credit Note |

|---|

| Nature of the document must be indicated prominently, such as ‘revised invoice’ or ‘supplementary invoice’ |

| Name, address, and GSTIN of the supplier |

| A consecutive serial number containing only alphabets and/or numerals, unique for a financial year |

| Date of issue of the document |

| If recipient is registered- Name, address and GSTIN/Unique ID number of the recipient |

| If recipient is unregistered- Name, address of recipient and address of delivery, with state name and code |

| Serial number and date of the original tax invoice or bill of supply |

| Taxable value of the goods or services, rate of tax and the amount of tax credited or debited to the recipient |

| Signature or digital signature of the supplier or his authorized representative |